Award-winning PDF software

Circular 230 Tax Professionals | Internal Revenue Service: What You Should Know

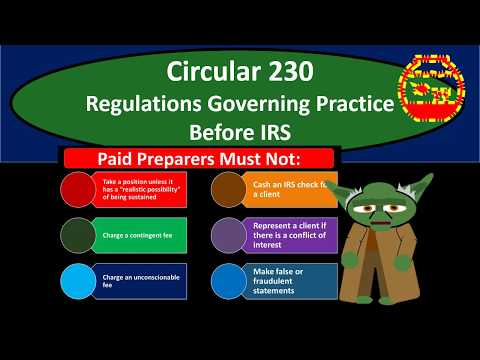

The IRS and its component agencies have adopted this regulation pursuant to Executive order 11246, “Prohibited Discrimination in Employment and Reemployment”. — The document is published under the authority of section 1136 (1)(A) of the Internal Revenue Code of 1986, as amended. — This regulation replaces guidance from the U.S. Department of the Treasury's Office of Professional Responsibility and requires that all attorneys, certified public accounting firms, enrolled agents, enrolled retirement account plans, and enrolled retirement compensation plans must adopt the following regulations: — The title page of the statement is the official statement of the position of the firm; — The statement must include the firm's name, address, telephone number, and electronic address; — The statement must identify itself as a statement of position of the firm's attorneys, certified public accountants, enrolled agents, enrolled retirement plan plans, and enrolled retirement compensation plans and certify that the firm is duly established and its management is competent; — This statement must identify the firm's address, telephone number, and electronic address; — The statement must clearly designate each practice area or division of the firm and the name of the person in charge; and the statement must identify the jurisdiction in which that person is registered and the firm's principal office. Circular 230: Requirements for Firms, and Information for Tax practitioners — Any tax practitioner is presumed to be a tax professional for purposes of Circular 230 if, in administering his or her business or profession, he or she does any of the following: — Fills out forms or participates in consultations for taxpayers, including tax examiners; — Fills out any other documents or materials in the taxpayer's case that support or address the taxpayer's tax issue or question; or — Does anything that the IRS considers related to the services to be performed for the taxpayer. — A tax practitioner's actions and statements are protected from liability under Circular 230 and the regulations. — A tax practitioner does not need to provide a “tax return preparer” classification to become a tax professional.

Online solutions make it easier to to arrange your doc administration and improve the productivity of the workflow. Carry out the fast guideline so as to complete Circular 230 Tax Professionals | Internal Revenue Service, stay away from mistakes and furnish it inside a timely manner:

How to complete a Circular 230 Tax Professionals | Internal Revenue Service on the web:

- On the website together with the kind, simply click Get started Now and move into the editor.

- Use the clues to complete the pertinent fields.

- Include your individual facts and make contact with knowledge.

- Make certain that you just enter suitable information and quantities in suitable fields.

- Carefully examine the content belonging to the type in the process as grammar and spelling.

- Refer to help part when you have any questions or deal with our Support group.

- Put an digital signature on your Circular 230 Tax Professionals | Internal Revenue Service with the support of Indication Software.

- Once the shape is completed, push Carried out.

- Distribute the completely ready sort by way of electronic mail or fax, print it out or save with your product.

PDF editor enables you to make improvements towards your Circular 230 Tax Professionals | Internal Revenue Service from any world-wide-web related equipment, customise it in line with your needs, sign it electronically and distribute in several options.

Video instructions and help with filling out and completing Circular 230 Tax Professionals | Internal Revenue Service