Award-winning PDF software

Circular 230 authorizes lisa to sign Form: What You Should Know

The IRS is required under Circular 230 to investigate the circumstances of the matter, taking into account all relevant facts, circumstances, and information. The IRS may revoke any registration when it determines that a disqualified person does not meet the requirements of Circular 230 (Circular 230.2, IRC 6103) (See “Disqualification: The IRS's Discipline Rules”). ‥ The IRS has the authority to impose a forfeiture on any taxable year in which a taxpayer is found to have willfully violated the IRS's Taxpayer Compliance Programs. ‥ If the taxpayer fails to pay the IRS the amounts due within 12 months after a Notice of Penalties is issued, and the taxpayer files subsequent and timely claims for refund or to correct a return or claim, the agency will take certain actions (See “Payable within Twelve Months — IRS”). 2. The IRS, via the Office of the Inspector General, conducts a review of the matter. 3. At the conclusion of its review, the IRS determines that the matter has sufficient facts to satisfy the following conditions: a. There is sufficient substantiation to support the claim for a penalty, deficiency or interest; or b. The taxpayer has willfully violated the IRS's Taxpayer Compliance Programs. 4. At the conclusion of its investigation, the IRS also assesses a civil penalty, as well as interest based on the amount of the penalty. a. Amount of penalty — Based on a three-year schedule for civil penalties, and penalties of 10 percent of the penalty amount for subsequent violations of the Internal Revenue Code (IRC Sections 6201(a), 6201(b)(1)(A), 6201(b)(2)), a maximum total penalty equal to 50 million must be assessed against the taxpayer, and interest at the prescribed rate (currently 2 percent per year); Other penalties may be assessed upon the filing of a certificate of deficiency or the return of income. 5. The taxpayer is not entitled to refunds or a refundable credit because of any violation of IRC Section 6103 or any other IRC provision. ‥ In some circumstances, a taxpayer (for example, one who files a Form 8300 on or after April 17th, 2015, or who provides an invalid taxpayer identification certificate) may not file Form 8300 and may be required to pay the penalty in excess of the 50 million.

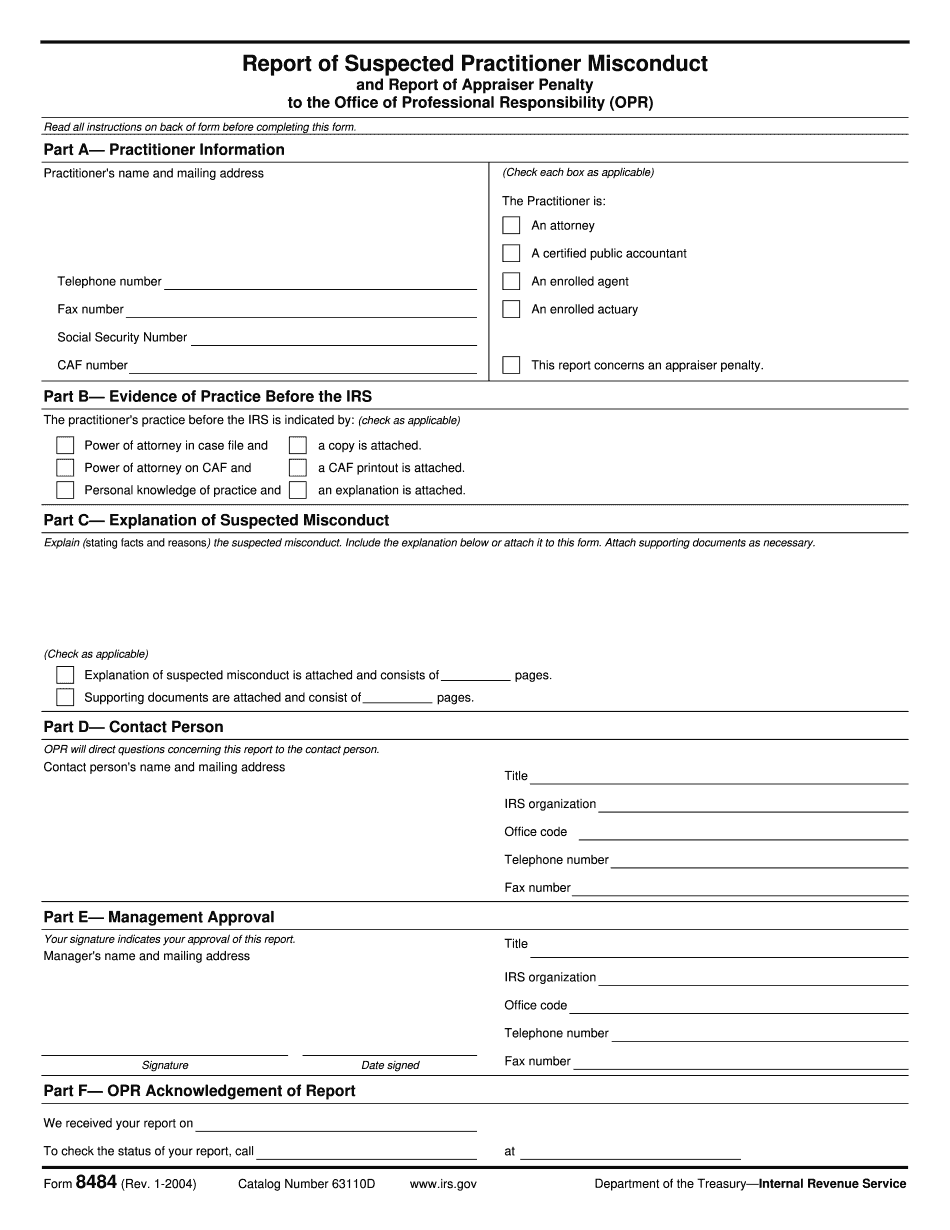

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 8484, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 8484 online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 8484 by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 8484 from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.