Hi, I'm Karen Hawkins, the former director of the IRS Office of Professional Responsibility. I will be your tour guide for the upcoming webinar "Shades of Grey: Practicing Before the Internal Revenue Service Circular 230 - The Current State". This webinar will be an update on the federal ethics rules for tax practitioners. There are several reasons why you should listen to this webinar. Firstly, Circular 230 has not been updated since 2014. During this time, there have been changes to the statute, regulations, and cases that have impacted the jurisdiction of the OPR. By attending this webinar, you will be able to obtain the information you need to understand the expectations that OPR has for practitioners practicing before the Internal Revenue Service. This is the only place where you will get this crucial information. Don't miss out on this opportunity to stay informed and up-to-date with the latest changes in the field. Join us for the "Shades of Grey: Practicing Before the Internal Revenue Service Circular 230 - The Current State" webinar.

Award-winning PDF software

Circular 230 email disclaimer 2024 Form: What You Should Know

CIRCULAR 230 DISCLOSURE STATEMENT Notice of Recommendation of the Office of Professional Responsibility | Internal Revenue Service May 14, 2024 — This circular contains guidance to practitioners on the removal of Circular 230 from their email footers and in Internal Revenue Service Circular No. 230 | Information -- AICPA Notice of Recommendation of the Office of Professional Responsibility | Internal Revenue Service August 4, 2024 — This circular contains guidance to practitioners on the removal of Circular 230 from their email footers and in Internal Revenue Service Circular No. 230 | Information -- AICPA Notice of Recommendation of the Office of Professional Responsibility | Internal Revenue Service March 14, 2024 — This circular contains guidance to practitioners on removing the text from their email footers and to Integral Tax Services | Internal Revenue Code Effective Date: March 11, 2020, Notice of Change to Section 708: A Guide for Taxpayers With Respect to the IRS Response Time | Internal Revenue Service September 21, 2024 — This circular explains that the IRS response time will be extended for certain categories of taxpayers in 2024 unless a taxpayer files an informal appeal. CIRCULAR 230 DISCLOSURE STATEMENT A practitioner may, with IRS approval, notify any taxpayer who resides or has a substantial business presence in the territory in which the practitioner is registered for purposes of this circular. CIRCULAR 230 DISCLOSURE STATEMENT A Taxpayer's Notice of Claim for Refund due to Failure to File an IRS Form W-9; or an Extension of Time to File a W-9 will be automatically posted to the practitioner's computer and sent to the taxpayer's U.S. address by the tax practitioner. This Notice (for purposes of section 872(h) of the Internal Revenue Code) shall appear as Exhibit S to the practitioner's tax return. Notice of Change to Section 708: A Guide for Taxpayers With Respect to the IRS Response Time | Internal Revenue Service May 28, 2024 — This circular explains that, for the 2024 tax year, taxpayers who have received a notice from the Internal Revenue Service and are unable to appeal or have filed an appeal within 45 days must respond to the notice in accordance with this notice in order to be eligible to receive a refund.

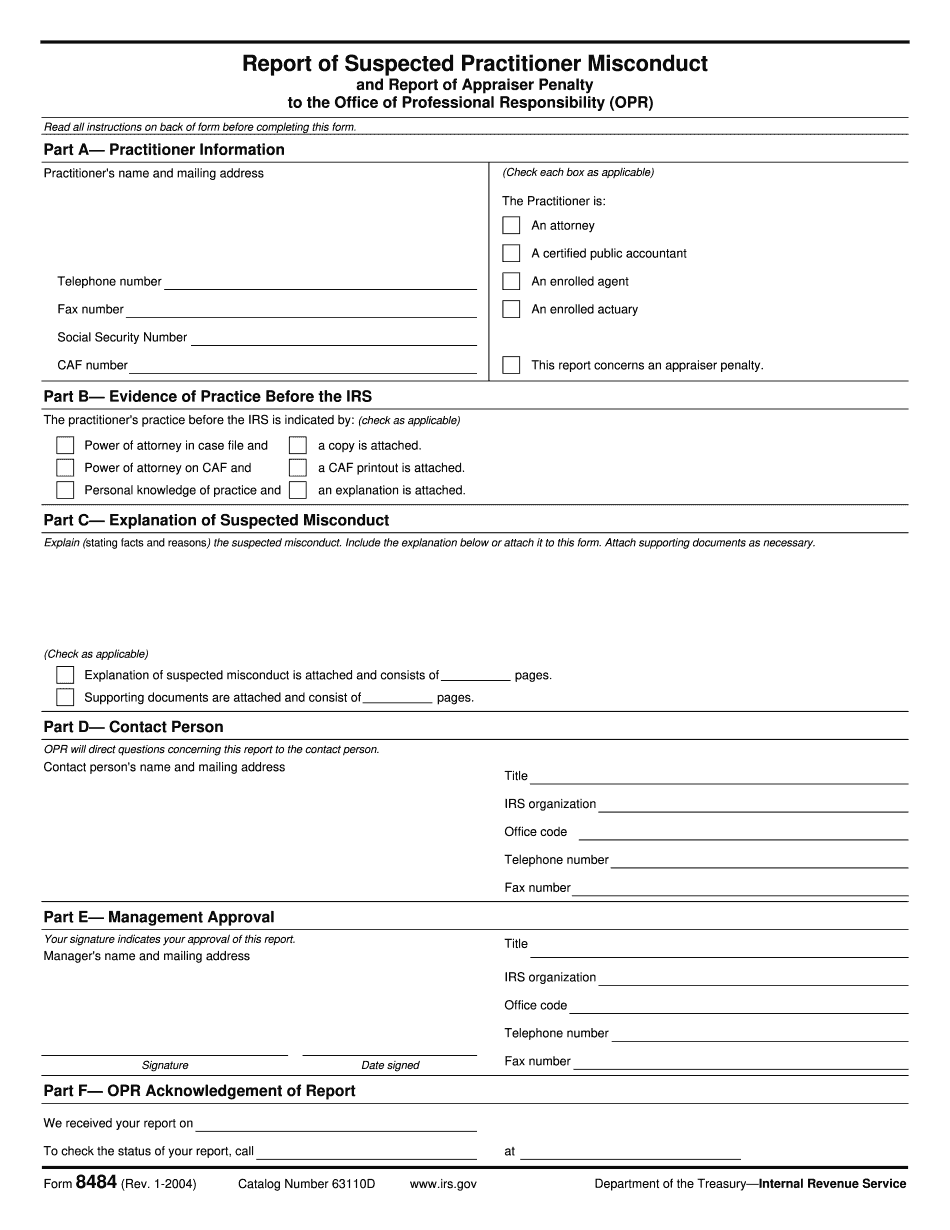

Online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 8484, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 8484 online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 8484 by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 8484 from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Circular 230 email disclaimer 2024